Understanding your Civil Society Organisation’s finances is essential to guarantee proper decision-making in your organisation’s activities and to ensure that your financial operations and processes are in line with the financial and accounting guidelines and principles. It can also ultimately support the sustainability of your organisation as a whole.

This Financial Management Guide is a basic tool to assist accountants and financial managers with making well-in- formed decisions regarding CSO management.

This guidebook was developed as part of “Ta’cir - Towards an Active Participation of Civil Society in The Reform Process” implemented by ACTED in partnership with Lebanon Support, Akkarouna, and Sheild, and funded by the European Union. It is published as part of the Civil Society Incubator, a programme by Lebanon Support.

Introduction

Understanding your Civil Society Organisation’s finances is essential to guarantee proper decision-making in your organisation’s activities and to ensure that your financial operations and processes are in line with the financial and accounting guidelines and principles. It can also ultimately support the sustainability of your organisation as a whole.

This Financial Management Guide is a basic tool to assist accountants and financial managers with making well-informed decisions regarding CSO management. After reading the Financial Management Guide, the organisation’s financial and accounting team should have:

-

Developed an improved understanding of the CSO’s finances, by recognising the need to secure cash and funding to meet the Organisation’s evolving requirements, enhanced its ability to review and interpret financial data and information, and prepared plans related to the Organisation’s operations.

-

Developed a process to document and update financial information for the Organisation’s financial operations.

-

Improved its ability to link other CSO management elements (such as fundraising) with the organisation’s financial management.

-

Set appropriate control standards for all financial and accounting activities.

-

Identified financial policies and procedures.

-

Ensured the continuity of financial tasks, by providing a reference guide for all financial functions and procedures.

-

Identified the administrative division’s tasks.

By fulfilling each of these objectives, the CSO should be able to make better-informed decisions and have an improved ability to monitor its financial performance in order to ensure good financial management.

The guide will also enable you to understand your organisation’s unique goals in order to develop a risk management plan, thus allowing you to anticipate unexpected issues or shifts in your plans.

Section 1: Identifying Financial Management Tasks and Accounting System Standards

Accountant:

The accountant, or their representative assigned by the Board of Directors (BoD), shall undertake the following financial and accounting procedures:

-

Prepare monthly and bi-annual financial reports and statements.

-

Produce cheques for operational expenses and project activities.

-

Develop financial account records for review.

-

Register all accounting records on a daily basis and submit them to the person or authority assigned by the organisation.

-

Carry out the organisation’s purchases, according to the purchasing policy.

-

Prepare payments related to the organisation’s management and projects, and ensure the availability of all documents related to these payments and their conformity with the standards set out in the relevant policies.

-

Obtain the approval of the financial manager and the treasurer, or of the person or authority assigned by the Board of Directors, on these payments.

-

Prepare and pay monthly salaries, as well as income tax and social security deductions.

-

Prepare bank reconciliations every month or twice a month, as necessary.

-

Audit the petty cash fund transactions, and prepare the related instalment.

-

Produce the organisation’s files and records for the internal and external auditor, if any.

-

Enter all financial data into the accounting programme.

-

Keep all financial files and statements.

Treasurer:

The treasurer is the person assigned and entrusted with the management of cash operations, such as revenues and expenses. They shall undertake the following tasks:

-

Receive cash from revenues and deposit it in the bank within the specified period.

-

Sign cheques/wire transfers, along with the Head of the Board of Directors or the person appointed by the BoD.

-

Monitor the financial system and supervise its implementation.

-

Assist with updating financial policies, in order to support oversight procedures and the internal control system, and submit these amendments to the BoD for approval.

-

Ensure the submission of periodic financial reports, as well as audited annual reports, to the BoD.

-

Assist the Organisation’s management and employees with preparing the annual budget, and ensure its submission to the BoD for approval.

Accounting System

The accounting system should meet the following minimum standards:

-

Full and accurate disclosure of current financial results for the organisation’s activities.

-

Records and books that adequately identify the sources and uses of funds related to different activities.

-

Effective control of all funds, properties and assets.

-

Comparison between actual costs and the budget for every activity.

-

Accounting records with all supporting documents.

Document Security and Protection

All documents should be kept in a safe and secure place, including:

-

Annuals accounts and revision and auditing reports.

-

All agreements concluded with the organisation.

-

Employment contracts, lease contracts and property deeds.

-

Correspondence with banks, donors, consultancy firms and others.

-

Any other document of financial or legal significance.

Section 2: Understanding the Finances of Non-Profit Civil Society Organisations

CSOs can and do make money in the same way as for-profit organisations. The difference is that funds earned by non-profit CSOs must be directed towards their previously set missions, vision, and activities. Therefore, a key element of CSO financial management is using surpluses to further organisational goals, rather than distributing them amongst shareholders.

In general, competitiveness exists between organisations, particularly given the scarcity of resources and cash donations. Thus, organisations should make good use of their financial resources in order to reach the highest possible number of beneficiaries. They should not use these resources in an uninformed way that does not provide the best social and service returns.

As such, minimum standards should be set to identify, analyse, measure, record, classify, summarise and disclose financial transactions, and produce an impact from the organisation’s operations, events and circumstances during the project implementation period. Reports should also be prepared and submitted to the financial department or the BoD, and written standards, policies and principles should be set and adopted to ensure the proper use of assets, in accordance with public service objectives, and to meet the targeted group’s needs.

Accounting principles should also be suitable for the organisation, given that the nature of activities and tasks differs amongst organisations, especially the accounting structure, which varies depending on the nature of the organisation’s projects, targeted group and needs, as well as the implementation period. In addition, the donors’ conditions and templates, based on which the work is to be performed, differ from one organisation to another and should be taken into account.

If the organisation does not abide by clear and written financial policies and systems, it may become exposed to several risks, such as:

-

Non-continuity of financial and cash functions within clearly-defined rules.

-

Forgery of financial documents and development of flawed reports.

-

Theft or embezzlement of funds.

-

Depletion of cash and liquidity.

-

Use of funds for purposes other than the set objectives.

-

Compromising the organisation’s reputation among donor institutions, beneficiaries, other organisations and partners.

The aim of establishing a transparent accounting system is to provide information for several purposes, such as:

-

Providing information for administrative purposes.

-

Providing necessary information to ensure the proper use of resources according to the set programmes and plans.

-

Providing necessary information to ensure the implementation of the established rules and provisions.

-

Provide necessary information to establish an accounting system that includes necessary accounting procedures, such as documents, records, etc., in order to facilitate control processes.

-

Compare revenues and expenses, and identify the difference between them for the purpose of decision-making.

-

Provide information to ensure the proper use of accounting procedures.

-

Provide information to ensure compliance with the adopted accounting rules and principles.

Organisations have financial and economic aspects, in addition to their other activities. They may require the adoption of accounting systems to safeguard their money, list debtors and creditors, disclose their financial position, and assess their role in performing services and providing goods to their beneficiaries in the best possible way. Thus, they represent a social structure based on cooperation and designed to facilitate individuals’ performance towards achieving objectives and building a better society.

As a result, organisations are considered one of the main components of modern societies, given the essential role they play in the social, cultural, economic and environmental spheres.

Section 3: Financial and Accounting Documents and Policies

It is a structure of policies that allow for the organisation’s financial and accounting management, designed as a clear guide for future policies on preparing the organisation’s final financial statements, in accordance with international accounting principles and the laws and regulations established by relevant authorities. It also reflects the actual financial position of the organisation to relevant authorities.

These policies aim at setting the basic rules of the financial and accounting system, which is used by all workers within the organisation in their performance of all financial activities. They also aim at preserving the organisation’s funds and properties, establishing the rules for disbursement and collection and for internal monitoring and control, as well as ensuring the integrity of financial accounts.

General Policy:

-

Fiscal Year: The organisation’s fiscal year is equivalent to one Gregorian calendar year, starting from the 1st of January and ending on the 31st of December of every year.

-

With regard to projects: The project duration and deadlines proposed by the donors should be respected. Revenues and expenses may overlap in more than one fiscal year. However, the donors’ reports should be prepared according to the duration and template proposed by the donor.

-

The organisation should follow the double-entry method in authenticating financial operations and accounting records.

-

Annual financial reports: Financial reports should be prepared and audited by the organisation as well as by an external auditor.

-

The organisation’s authorised signatory should be appointed by the BoD, according to the list of powers applicable within the organisation, and as established in the regulations for signing on behalf of the organisation. This should include:

-

Limitations of financial expenditure operations.

-

Adopted signature templates with their effective dates.

-

-

Cash consists of the available cash in the fund and the amounts deposited in banks and bank accounts.

-

The organisation should specify the main currency used for recording financial operations and preparing reports.

-

When using a foreign currency, the official exchange rate issued by Lebanese authorities on the specific date should be adopted.

-

Account balances of activities (revenues and expenses) should be translated into the foreign currency according to the average exchange rate for the duration of the report.

-

The chart of accounts should be prepared by the financial management and the external auditing firm, according to the financial laws in force in Lebanon, and becomes effective for use by the accountant.

What are the key financial documents for CSOs? Financial Documentation 101

The key to successful financial management is the detailed tracking of documents, which means recording and tracking every past, present and future activity. In order to ensure good financial documentation, the CSO should have a robust system that records every financial activity.

Accounting Procedures Manual: The executive team must develop and adopt a set of procedures on how the CSO manages its finances, which impacts the way activities are carried out by the organisation. The financial team usually coordinates the executive team’s responsibilities with regard to the manual, including regular revisions and updates thereof. The organisation should make every effort to ensure compliance with the manual procedures.

Member registration book and membership fees: Provides a cumulative record of all the members who have settled their membership fees and all members with outstanding fees.

Record book containing the meeting minutes pertaining to financial resolutions: Tracks progress and decisions made with regards to the CSO’s financial obligations.

Record book containing files related to financial by-laws and accounting: Assists the treasurer in maintaining accounts and records expenditures based on by-laws.

Cheque book: Keeps track of withdrawn money and payee details.

Bank passbook: Keeps track of the funds available and/or used from the organisation’s account.

Cash book: Maintains a record of the cash in hand.

Ledger book: Maintains a record of incoming and outgoing funds.

Stock book: Details moveable and immoveable assets owned by the organisation.

Receipt book: Provides acknowledgment of received funds/donations.

Budgets (financial forecasting): CSOs should have an operating budget (or annual budget) outlining the upcoming year’s planned revenue and expenses. Budget amounts are usually divided into major categories, such as salaries, profits, IT equipment, and office supplies. For effective planning, CSOs should also have cash budgets that outline the movement of cash expected to be received and paid over the short-term, such as over a one-month period. Moreover, organisations should develop a programme budget, which is a budget for each major service provided by the CSO to its members. Planning and tracking financial costs for each programme is critical, as CSOs should strive as much as possible to minimise overhead (or administrative) costs – in other terms, administration and maintenance costs.

Petty cash book: A petty cash fund can be used for covering minor expenses, such as the purchase of cleaning supplies. One can withdraw money from the fund by recording who took the money, the amount taken, the purpose, and the date of withdrawal in a designated ledger.

Financial reports: This report’s type and frequency depend on the CSO’s nature and situation. Usually, each donor agency requires progress reports and end of project financial reports. Other internal reports ought to be prepared for the project managers, the executive team, and/or the Board, usually on a yearly basis for the latter.

Financial Policies and Practices

Policies are the laws that govern and organise CSOs. Without organisational policies governing the CSO’s daily financial procedures, your organisation will be inconsistent in its planning and work, and thus ineffective. Therefore, the establishment of a well-prepared set of financial policies is the key towards maintaining your desired financial position.

Checklist: Establishing Financial Policies

In order to establish financial policies, your CSO must first determine the financial objectives it wishes to achieve and consider the areas in which policies can be established. Areas for which policies could be established include, but are not limited to, the following:

-

Liquidity target policy

Limitation on the number of months of expenses held in cash reserves (typically a minimum of three months, but normally at least six months, is prudent);

-

Accounting policies

Cash basis or accrual basis, and accounting standards used;

-

Cash management policies

Cash collection and receivables, cash access and wire transfer policies, and cash disbursement and payables;

-

Cash forecasting policies

Method of forecasting, to whom forecasts are distributed and in what timeframe;

-

Banking relations policies

Method of bank selection and limitation on maximum account balance;

-

Insurance and risk management policies

Specific identification of all the risks and how these will be monitored, and limitations on the types of insurance policies that will be used and coverages that will be carried;

-

Purchasing policies

Restrictions on the bidding process and on final vendor selection and pricing;

-

Financial planning and budgeting policies

Development of operating budget and frequency of higher management (or Board, depending on the CSO’s statutes and regulations) review of budget figures versus actual figures;

-

Investment policies

Short-term and long-term investment policies;

-

Debt/borrowing policies

Limitation on short-term and long-term borrowing, and allowable & unauthorised uses;

-

Internal controls and reporting policies

Conflict of interest policy and fraud prevention policy;

-

External reporting policies

Donors, grantors, community, regulatory authorities, and other;

-

Fundraising policies

Donation use and receipt, use of time-bound or purpose-bound funds, and policy to solicit unrestricted donations.

The development of effective policies and procedures is no easy task. If you do not have an experienced staff member willing to devote time to this endeavour, you may decide to network with other non-profit CSOs that can assist you in developing a solid set of policies to be tailored as need be.

Many policies are determined internally by the management of your CSO; however, others can be decided externally. Gaining a deeper knowledge of external policies, such as those demanded by donor or governmental agencies, will help you determine which internal policies should be developed or modified. After establishing policies, your CSO can then develop procedures in compliance with them.

Section 4: Cash Management

Cash management holds special importance with non-profit CSOs, as those with insufficient cash may risk focusing on solving their financial problems rather than fulfilling their mission. Thus, your CSO should have liquidity – that is, it should have enough cash to cover expenses.

Tips on Cash Management:

Cash and bank account management is considered one of the most sensitive issues that are subject to accountability. Therefore, it requires the following control and monitoring procedures:

-

The employee who is authorised to receive cash and cheques is the only person who is allowed to do so.

-

Personal funds should not be confused or mixed with the organisation’s funds.

-

Cash and cheques should be kept in a secure place (a safe if possible). The safe should be installed in a place where it cannot be moved, making it difficult to access.

-

Available cash should be deposited with the treasurer at the bank, in accordance with the depositing policy referred to in the Cash Management section. In return, a proof of deposit (deposit slip) is obtained from the bank. The person in charge should keep the deposit slip and the documents proving the amount received.

-

A cash expenditure limit should be specified according to the organisation’s workload. Cheques are prepared for any amount that exceeds the maximum amount of monthly expenditure.

-

Cheques should have two out of three signatures, should be marked with the phrase “To be paid to the primary beneficiary,” and should be crossed.

-

The persons authorised to sign a cheque should not sign any before filling all required information thereon.

-

Cancelled cheques should be kept in the cheque book and recorded in the cheque movement record.

-

Cheque books should be ordered officially after the authorised persons sign the request. A specific person will be duly appointed to receive cheque books from the bank, which are kept in a secure place. The said person shall sign an acknowledgment of responsibility in the event that a cheque is lost from the cheque book. The bank should also be immediately notified to stop lost cheques from being cashed.

-

Persons authorised to disclose the organisation’s account activity from the bank should be identified by an official letter, a duly signed copy of which is submitted to the relevant banks.

-

Fully used cheque books should be kept in a secure place, for a period no less than 5 to 10 years.

-

The accountant should produce a monthly table of prepared cheques based on the template shown below.

-

Cheque books should be used in a sequential manner by number. More than one cheque book may not be used for the same account at the same time.

-

Bank reconciliations should be prepared at least once a month, according to cheque movements within the organisation, and necessary reconciliations should be carried out.

-

The tasks of the treasurer should be separated from the tasks of the accountant (financial officer).

Table of Prepared Cheques for the Month of __________

|

# |

Account No. |

Bank/Branch |

Cheque No. |

Item Description |

Name of Beneficiary |

Date of Issuance |

Cheque Amount |

|

1 |

|||||||

|

2 |

|||||||

|

Monthly Total |

|||||||

Template of Monthly Bank Reconciliations

|

Balance |

|

|

Plus: |

|

|

Revenues: |

|

|

Total available funds: |

|

|

Minus: |

|

|

Bank commission: |

|

|

Total cheques: |

|

|

Remaining balance: |

Cash Receipts:

The rules of cash receipts are as follows:

-

The treasurer should receive cash from different sources, depending on the organisation’s activity.

-

The treasurer should issue a document for all cash receipt operations in two copies, using the accounting system and in writing.

-

The treasurer should deposit cash holdings in designated banks after verification and auditing by the accountant.

-

The accountant should record depositing operations based on the bank deposit card in designated accounts.

-

Cash should be kept in a secure place.

-

The treasurer should prepare the monthly receipt table according to the following template:

|

# |

Date |

Name of Recipient |

Number of transfer or receipt |

Source (Project Name) |

Amount |

|

1 |

|||||

|

2 |

|||||

|

Monthly Total |

|||||

The aim of a petty cash fund is to keep a sufficient amount of cash, which is relatively small, to settle small recurrent expenditures, such as: hospitality, gas, local transportation, mail, drinks (coffee and tea, sugar, etc.), cleaning supplies, and other expenses.

-

The petty cash fund remains in the custody of the accountant.

-

Petty cash fund payments are issued from the organisation’s general bank account, via a cheque or through cash withdrawal.

-

The organisation identifies the petty cash limit based on its needs.

-

The organisation specifies the nature of petty cash expenses.

-

The accountant pays the petty cash and keeps the documents that prove these expenses.

-

If the payment limit is to be exceeded, a written permit must be obtained from the relevant managerial level.

-

Petty cash funds and received revenues should not be mixed. They must be kept separate.

-

The petty cash fund treasurer should record the payments in the petty cash record first, and check the remaining balance before disbursement.

-

The accountant and treasurer should reconcile petty cash expenses on a monthly basis, and should sign the petty cash table and keep all documents that prove the expenditure.

-

The accountant should seal all invoices and documents with the word “paid”. The nature of the project related to this expenditure should be identified.

-

The amount taken from the petty cash fund shall be reimbursed in order to keep the same balance in the fund.

Petty Cash Table for the Month of __________

|

# |

Date |

Nature of Expense |

Invoice No. |

Item Description |

Amount |

|

1 |

|||||

|

2 |

|||||

|

Monthly Total |

|||||

Treasurer: Signature:

Bank Accounts

Registered CSOs require operating bank accounts for two main reasons: First, a bank account is essential to receive funds from donors, and, second, a bank account is a secure and transparent method for storing and transferring money. CSOs need to understand how to carry out bank transactions and what corresponding procedures need to be included in the CSO’s regulations to guide such transactions.

Bank accounts should reflect the organisation’s financial transactions. To prevent loss (due to mismanagement, corruption, or human error), it is preferable to process the majority of transactions through the bank. This requires timely depositing of funds received and making payments through a cheque book or with documented cash transactions.

Policies for Handling Bank Accounts

The following policies should be followed when carrying out any work related to bank accounts:

-

Open all bank accounts in the name of the organisation.

-

Sign all issued cheques by the people authorised to do so according to the list of financial and administrative powers within the organisation.

-

Carry out reconciliation operations for all bank accounts on a monthly basis.

-

Resolve all outstanding issues that arise during reconciliation operations, and investigate them as soon as they appear.

-

Carry out all bank transfers related to the organisation.

-

Close any account according to the adopted procedures.

What does a financial manager do?

The financial manager is responsible for the finances, assets, and liabilities of the CSO. He/she assists the executive team in protecting the financial integrity of the organisation, advises and assists the management in fiscal responsibility, and ensures that the organisation’s strategic objectives are financially viable.

In particular, a financial manager:

-

Works closely with the director of the CSO and its executive team;

-

Gives financial recommendations to the director of the organisation and its executive team;

-

Presents the director of the organisation and its executive team with budget statements, accounts and financial information at all key points in the planning and budget cycle. The key issues in these statements are outlined in a coherent and easily understandable way;

-

Participates in fundraising efforts and events;

-

Consults with the director of the organisation and its executive team regarding financial assumptions underlying planning and budget documents, and advises on accounting and budgeting in line with the goals of the organisation;

-

Ensures proper procedures for preparing, auditing, and presenting the annual reports are followed;

-

Ensures appropriate accounting procedures and controls are in place throughout the organisation;

-

Acts as a member on the audit committee, if it exists;

-

Ensures recommendations made by external auditors are implemented;

-

Carries out the responsibilities entrusted to them in accordance with the bylaws and statutory requirements of the CSO;

-

Depending on the bylaws of the CSO, the financial manager may be required to coordinate with the treasurer of the Board.

CSOs receive financial support from donors and logistical support from volunteers. Their operations must be transparent in order to guarantee the trust of the general public and society. Therefore, CSOs must keep all documents and give clear and transparent access to them to the general public, by providing information on its mission, administrative structure, periodic programme and performance reports, and financial reports.

Section 5: Managerial Structure, Responsibility and Ethics

The success of a civil society organisation (CSO) depends on its structure, policies and the methods it uses to accomplish its mission. Its main characteristics are ethics, governance, transparency and honesty, and, most importantly, its financial architecture. While it is generally understood that the Board’s main responsibility is strategic leadership, and that the organisation’s management is the responsibility of its manager in cooperation with its executive team, this responsibility might change in accordance with its bylaws and regulations.

Internal Control

The CSO's financial architecture is further strengthened by the adoption of a system of internal controls that dictates operations and delegates responsibilities to prevent abuse of power and achieve organisational goals in an effective and transparent manner. This system helps the organisation deal with daily risks related to errors, confusion or fraud, and protects the team from any pressure arising from misuse of funds and suspicion of misconduct.

There are two important aspects of an internal control system: the control environment and the control procedures that take place within this environment.

- Control environment: The control environment includes management style, organisational values and culture. The ideal control environment must lead to fair and transparent practices. Does the administration lead by example? Is employment fair or is there favouritism? Is priority given to motivation, training and internal audit? Are the procedures written and distributed to workers?

- Control procedures: Almost all internal control procedures fall into one of the seven categories below:

- Physical verification: counting funds, verifying and counting assets;

- Restricting access: locks, passwords, and bank signatories;

- Standard documents: standard formulas for reception and delivery receipts, local purchase orders and requests, schedule for signing travel authorisations, etc.

- Dividing duties: ensuring that the person who is able to make a transfer from start to finish is not the same person who reviews and gives permission to carry out the transaction. For instance, we may sometimes see this in the procurement process;

- Cheques and budgets: manual cashbook budgeting, dual monitoring of account books, and review of bank balance reconciliation;

- Approval and allowance: budget holders’ agreement to payments, Board authorisation to dispose of assets, etc.

- Reconciliation: comparison of the bank disclosures and cashbook, and matching between your own records and the disclosures issued by the provider.

Effective financial management also ensures internal control:

-

Budgeting: verifying the budget before making a payment is an important control over spending.

-

Accounting: transparent record-keeping is an important control against fraud.

-

Reporting: the review of financial reports is an important control for detecting errors and non-conformities.

Potential Internal Control Procedures

Below is a list of potential internal control procedures:

Delegated Authority:

The Board gives the executive director the power to carry out the daily work of the organisation. The director can also delegate authority to team members, allowing smooth workflow in the absence of key personnel. This is written in a delegation document that is reviewed on an annual basis to ensure compatibility with the needs of the organisation. This document should also highlight delegation arrangements to cover the absence of key personnel. Violation of the delegation of authority are a serious issue and should be dealt with accordingly.

Bank Reconciliation:

The final budget for the passbook must be reconciled according to the closing balance of the bank statement at the end of each month. This important control procedure allows the organisation to identify errors and omissions in its records, as well as detect cheque frauds, bank errors and even bank fraud. A bank reconciliation statement must be prepared for each bank account every month, before being reviewed and signed by another official, such as the manager or treasurer.

Cheque Signature:

The CSO's bylaws and regulations determine the persons authorised to sign cheques. Some organisations may decide that there must be two signatories for expenditures exceeding certain amounts, and it is important that signatories carefully review the documents. Blank cheques must not be signed in advance, as this challenges the goal of maintaining the principle of accountability.

Fixed Assets:

Fixed assets include: maintaining a record of the assets, periodically checking the existence and status of the assets, and establishing policies to allow asset disposal. When the CSO is large, it may also be necessary to track the movement of assets between departments (with an asset transfer form), and to hold the department heads responsible for the assets.

Maintenance:

Regular maintenance (e.g. for buildings and equipment) improves safety and extends the lifespan of assets. Therefore, preventive maintenance policies must be strengthened to ensure regularity of services. For instance, buildings can require a professional and programmed maintenance contract, and a realistic budget must be established for that purpose. Qualified technicians should also regularly maintain office supplies, such as photocopiers and electrical equipment.

Section 6: Understanding Accounting Principles and Financial Statements

The financial statements and the budget versus current reports help demonstrate the financial performance of your organisation and determine whether you are achieving your financial goals and accomplishing your mission, and they shed light on how this is done. The organisation's financial statements can be of significance to both internal and external audit, including staff, donors, beneficiaries, and tax authorities, among others. The trust of these actors in the organisation’s financial affairs is affected by the results and effectiveness of the programme, as well as the financial records, management and policies.

Accounting Standards

There are many accounting standards in the world, and each country is able to choose its own standards. The CSO must adhere to the accounting standards applied in the country it works in. For Lebanon, the accounting standards used are the International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board (IASB).

Fund-Based Accounting versus Accrual Accounting

In fund-based accounting, revenues are recorded when cash payments are received, and expenses are recorded when cash is released. In accrual accounting, revenues are recorded when the organisation receives them (e.g. when providing a service), and expenditures are recorded when they occur (e.g. when you have a cost related to the goods or services received). Accrual accounting provides a clearer picture of the operating results in a given time period. International Financial Reporting Standards (IFRS) are used on an accrual basis.

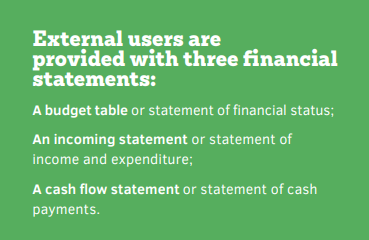

External Financial Statements

Budget Table

The CSO’s budget table shows what the organisation owns and what it owes, as well as its financial status at a given time. In the budget table:

-

Assets are the inventory owned by the CSO and used to implement programmes and provide services.

-

Liabilities are the amounts borrowed by the organisation and what it owes to suppliers.

-

Net assets include the amounts used when the CSO was first established, as well as the funds it has "acquired" over the years if the income exceeds the expenditures.

It is worth noting that assets (A) are always equal to liabilities (L) plus net assets at any given time. This is shown by the following accounting equation:

A + L = net assets

To determine profits, the following accounting equation is used:

A = L + OE (Owners’ Equity)

Put simply, every dollar of assets on the balance sheet must be funded either by a dollar of debt (borrowed funds) or by net assets (cumulative gains). Since non-profit organisations do not incur credit, their assets are determined by accumulated gains over the years. Any other asset growth must be funded by liabilities or debt.

Funding decisions include the need to borrow, in parallel with the amount requested. The accounts payable is a source of interest-free financing from suppliers, since most organisations benefit from the lending period granted to them. Moreover, some CSOs can borrow funds or use a credit line for short-term financing.

|

STAR NGO |

||

|

Statement of financial position |

||

|

June 30, 2016 |

||

|

Financial statements in USD |

||

|

Assets |

||

|

Current assets: |

||

|

Liquid funds: |

274,139 |

|

|

Donations and debtor contracts |

276,854 |

|

|

Prepaid expenditures |

17,000 |

|

|

Total current assets |

567,993 |

|

|

Properties and equipment |

||

|

Less: cumulative depreciation of $27,505 |

39,393 |

|

|

Other assets – security deposits |

12,000 |

|

|

Total assets |

619,386 |

|

|

Liabilities and net assets |

||

|

Current liabilities: |

||

|

Accounts receivable and expenditures |

179,578 |

|

|

Advances |

72,544 |

|

|

Total current liabilities: |

252,544 |

|

|

Net assets: |

||

|

Unrestricted: |

38,427 |

|

|

Temporarily restricted: |

328,837 |

|

|

Total net assets: |

367,264 |

|

|

Total liabilities and net assets: |

619,386 |

Income Statement

The income statement indicates the extent to which the CSO’s income exceeds its expenditures, or vice versa, in a given period of time. Income consists of contributions, donations and in-kind grants with interest received, and profit or loss in investments, as well as other sources of income. It is worth noting that some of this income unrestricted, some is partially restricted, and the rest is permanently restricted.

-

Unrestricted: contributions that are not subject to donor restrictions when using them.

-

Temporarily restricted: contributions made by donors with restrictions that may be lifted with time.

-

Permanently restricted: contributions from donors that are subject to restrictions in their use or purpose.

|

STAR CSO |

|||||

|

Income statement |

|||||

|

For the year ending on June 30, 2016 |

|||||

|

Financial statements in USD |

|||||

|

Unrestricted |

Partially restricted |

Total |

|||

|

Income and support |

|||||

|

Governmental contracts |

692,998 |

692,998 |

|||

|

Donations and contributions, non-governmental |

188,760 |

559,100 |

747,860 |

||

|

Fundraising event |

11,100 |

11,100 |

|||

|

Meeting programme restrictions |

333,930 |

(333,930) |

- |

||

|

Interest received |

3,915 |

3,915 |

|||

|

Total income and support |

1,219,603 |

236,270 |

1,455,873 |

||

|

Expenses |

|||||

|

Programme A |

357,953 |

357,953 |

|||

|

Programme B |

118,378 |

118,378 |

|||

|

Programme C |

381,238 |

381,238 |

|||

|

Programme D |

229,861 |

229,861 |

|||

|

Total programme expenses |

1,087,430 |

1,087,430 |

|||

The only way to ensure that you reach your liquidity goal is to manage the flow of incoming and outgoing funds carefully. The budget statement and the income statement do not show cash flow when drafted based on accrual accounting. In order to understand the financial position, we need to review the Statement of Cash Flow (SCF), which divides the cash flow into three categories:

-

Operation: cash received and paid as income and expenditures recorded in the income statement;

-

Investment: cash received and paid for the purchase and sale of long-term assets (fixed assets);

-

Financing: cash received and paid related to borrowing funds.

|

STAR CSO |

||

|

Cash flow statement |

||

|

For the year ending June 30, 2016 |

||

|

Financial statements in USD |

||

|

Cash resulting from operational activities: |

||

|

Change in net assets |

83,426 |

|

|

Corrections to adapt to change in net assets |

||

|

To net cash in operational activities: |

||

|

Depreciation |

8,946 |

|

|

Increasing grant and contract benefits |

(50,019) |

|

|

Increasing prepaid expenditures |

(3,932) |

|

|

Increasing security deposits |

(255) |

|

|

Increasing account benefits and cumulative expenditures |

120,217 |

|

|

Decrease in advances |

(6,394) |

|

|

Net cash provided by operational activities |

151,989 |

|

|

Cash payments derived from investments activities: |

||

|

Capital expenditures |

(9,573) |

|

|

Net cash used in investment activities |

(9,573) |

|

|

Net cash increase |

142,416 |

|

|

Cash – beginning of year |

131,723 |

|

|

Cash – end of year |

247,139 |

|

Section 7: Setting the Operating Budget and Cash Budget

The budget is at the core of successful financial management. A budget is a detailed financial plan drawn up in a specific currency. Before setting a budget, the CSO must determine its mission and goals and develop a strategic plan accordingly.

Budget structure: depending on the nature of its activities, the organisation can prepare the budget at several levels, based on its structure, and the budget can be arranged according to specific projects or programmes.

To ensure the effectiveness of the budget as a means of planning and evaluation and achieve its objective, it should be characterised by the following:

-

Clarity: since budget readers are many and their goals vary, the budget should be smooth and clear to readers without the need for any explanatory margins.

-

Timeliness: the budgeting process takes place across several stages before it is submitted to the Board of Directors for approval. It is recommended to start preparing the budget at least two months before the end of the current fiscal year.

-

Budget titles: the budget should be titled at the time of preparation, and the schedule of accounts used in the organisation should be taken into account. Moreover, the terminology should be standardised because the main elements of the budget will appear later in the books of accounts and administrative financial reports, which will facilitate the review and control process.

-

Estimating expenses: you should keep the details and clarifications related to the numbers mentioned in the budget to provide justification when needed. It is recommended to keep a record of all resources, the number of units, and the cost per unit.

-

Assumptions: when setting a budget, all assumptions used to create it should be attached thereto. Moreover, when preparing the budget and submitting it to administrative bodies for approval, the assumptions used should be provided as proof.

-

Emergencies: it is recommended to place an emergency item at the end of the budget, which is calculated on a proportional basis (5% to 7%) of the total estimated expenditures.

Tips: Preparing Annual Budgets

Before turning to the budget preparation mechanism, it must be emphasised that the success of the budget as a planning and control tool depends on the efficiency of the human element in preparing the budget in its various stages. A special committee called the "Budget Preparation Committee", which must be chaired by the treasurer of the Board of Directors, is assigned to draft the budget. Its members usually include representatives of the finance and accounts departments, the director of the organisation, and programme or project managers.

Major steps include:

-

Each one of the organisation's programme departments is responsible for preparing its own budget.

-

The accountant and treasurer should coordinate budget preparation activities in agreement with the chair of the Board of Directors and other relevant parties in the organisation, such as: the director of the organisation, or the parties tasked with preparing the annual budget.

-

The annual budget must be submitted to the Board of Directors for approval and validation within a period not exceeding mid-December.

-

It is preferable to separate the fixed assets budget from the operating expenditures budget.

-

Expenditures or payments outside of budget items may only be done after obtaining the written approval of the legally authorised party.

-

Credits may be transferred from one item to another after the written approval of the legally authorised party is obtained.

-

The annual budget is recorded in the financial and accounting management systems.

-

It is recommended that the budget be divided on a quarterly basis to facilitate the control process, thus allowing the necessary decisions to be taken to facilitate expenditure management.

Detailed Procedures for Preparing Annual Budgets:

|

Procedure |

Person in Charge |

|

Project/Programme Manager |

|

The Organisation’s Budget Committee |

There are two main ways to set the budget: incremental budgeting and zero-based budgeting. You can choose the most convenient approach according to your skills and available time:

-

Incremental Budgeting:

This approach supports any annual budget for current figures, and sometimes those observed during the previous year, allowing us to monitor inflation and known changes in activity levels. This approach has the advantage of being fairly simple and quick to implement, and is more beneficial to organisations that experience few changes from year to year. This approach is often criticised for not promoting innovative thinking and for perpetuating existing problems. Moreover, it makes it difficult to justify numbers related to donors since the original accounts can be forgotten with time.

-

Zero-Based Budgeting:

An alternative approach is to start with a blank page with a zero base. Zero-based budgeting (or ZBB) ignores past budgets, and begins with goals and activities for the coming year. ZBB requires the budget author to justify the requirements for all resources. This process can be convenient for CSOs that are experiencing a period of rapid change and whose income is based on the activities they carry out. This method of budgeting is believed to be healthier, as it is based on the details of the planned activities. However, it imposes a bigger workload on managers, compared to incremental budgeting.

-

Activity-Based Budgeting:

Activity-based budgeting is a special form of zero-based budgeting, which is often used in the CSO sector to set project budgets, and is preferred by many donors.

Budget Types

Budgets are divided into three types:

-

Income/expenditure budget/operating budget;

-

Capital budget;

-

Cash flow forecast/cash flow budget.

Operating Budget

The operating budget, or revenue and expenditure budget, establishes the costs anticipated for operating the organisation (or recurrent costs), and shows where the funds to cover costs will come from. Therefore, the budget oversees and foresees progress through planning and forecasting, often on a quarterly or monthly basis. When preparing an operating budget, the financial manager can consider questions such as: "How will we receive many donations and other income sources in the coming year?" or "How can we anticipate expenses based on our operating plans?"

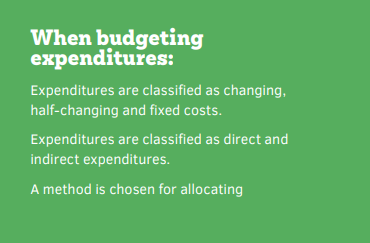

Before setting an expenditure budget, a reasonable amount of income must be estimated in order to establish an income budget. However, the expenditure budget must be independent of the income budget, and should be prepared before the income budget is completed.

Reactions in the current year regarding the reality of the past year up until now help estimate the proposed budget for the coming year. Operating budgets are mainly used to develop a plan for funds, anticipate possible problems and infer real performance (analysis of changes). The process of setting the operating budget must be done on a monthly basis throughout the year to avoid any surprises at the end of the year.

When developing an operating budget, the following should be noted:

-

Some items are estimated, while others are calculated.

-

Estimates include autonomy.

-

Calculations include finding a historical relationship between a variable (such as the number of hours during which your organisation uses electrical machines), the expenditure component (such as electricity), or deriving the historical rate of growth.

-

Capital Budget

The capital budget lists the expenditures that you intend to make in the coming year(s) in capital projects, and the single components that will become part of the CSO’s fixed assets. Since these assets typically involve significant expenditures and non-recurrent costs, it is best to list them and monitor them separately. Examples of capital expenditures include vehicles, office furniture, electronic equipment, and major renovations.

The effects of the operating budget, such as the operating costs of the machines, should be taken into account. There is no need to set a separate capital budget when the number of items to be purchased from the capital is limited to one or two items. In this case, it may be sufficient to include the capital-related items in a separate section of the operating budget; this is the most common method used in project budgeting.

Cash Flow Forecast

Cash reserves are essential for good financial management in the event of delayed grants or unforeseen expenditures. In fact, cash flow forecasts or cash flow budgets help managers determine when cash levels become critical. This includes predicting how cash will flow to and from the organisation during the year by dividing the main or total budget into smaller intervals, usually over the period of one month. While the budget for income and expenditures indicates whether the organisation is covering its costs throughout the year or not, the cash flow forecast indicates whether it has enough cash in the bank to meet all of its liabilities as they arise. Therefore, forecasting helps the organisation determine the potential lack of cash and avoid the following:

-

Requesting grants from donors early;

-

Delaying the payment of some bills;

-

Delaying activities; or

-

Negotiating a temporary loan from the bank.

Moreover, cash flow forecasting is useful when the CSO has a lot of cash that should be invested to maximise the return on investment.

In order to prepare the cash flow forecast, you need to collect all of the organisation's activity plans and budgets for the year. This process is better completed through an electronic spreadsheet software such as Excel. Simply put, the cash budget shows the funds expected to be acquired or spent, as well as the amount and duration of shortfalls and surplus cash in a given period of time (usually 12 months). It aims to determine instances of imbalance so that the financial manager can take early measures to manage the cash status.

The cash budget indicates the following:

-

The asynchronous nature of cash flow to and from the organisation;

-

The seasonality of flows (e.g. donations increase during Christmas and Ramadan);

-

The degree and duration of non-conformity (surplus or deficit).

Guidelines:

-

For each item of the operational budget, you need to forecast the flow of cash and plan it in the forecast statement. This depends on the timing of the expenses. Some activities are easier to predict than others (e.g. monthly salaries, annual audit fees), while certain transactions (e.g. repairs) cannot be foreseen.

-

After dividing the budget and allocating funds based on activity plans for each month, the net cash flow can be calculated; for example, incoming cash may be more than the cash released, or vice versa. It is common to enter an estimate of any bank budget created as a reserve, to help manage your cash flow.

Section 8: Financial Reporting

The Principles of Financial Reporting

After establishing accounting systems and budgets, the next step is to prepare financial reports in order to highlight and oversee the financial affairs of the CSO. It should be noted that preparing the financial report is not as time-consuming as you may think, as long as the accountants are knowledgeable and do not make mistakes. Financial reports must be issued on time and should be correct and relevant. They are initially requested by the director, executive team and senior management, as well as by existing and potential donor agencies.

When developing the annual financial accounting, information is summarised and addressed to the management accounts for internal oversight of progress in comparison to the budget. At the end of the year, the annual accounts (e.g. the budget sheet, the statement of income and expenditures, and the statement of cash flows) are ready to be transferred to the senior management, as well as to external stakeholders (government, and especially donors).

At regular intervals, the CSO will also be asked to complete reports on the progress of its work and submit them to donor agencies.

What are Annual Accounts?

The budget report, the statement of income and expenditures, and the statement of cash flow are necessary at this stage. This data should be prepared as soon as possible at the end of the fiscal year, within six weeks for example, according to the internal policies of the CSO, and must be ready for management and external auditing.

The annual financial statements, or annual accounts, together with the annual report, are important aspects of the CSO's ability to attract partners. Since many parties will be interested in annual accounts, the latter must promote the CSO and its work, meet the needs of the account user, and comply with the requirements of auditors.

Drafting Management Reports

Managers (project management, programme management, senior management, and executive management) need financial updates throughout the fiscal year in order to effectively oversee progress and budgets. If these reports are issued on time, problems can be addressed early and risks can be mitigated.

Management reports are compiled by taking summary numbers from the main accounting books and the budget for the same period. The preparation of these reports should not require additional work if the accounts and budgets use the same symbols and classifications, making it possible to organise and include them in a table of accounts. Ideally, these management reports, also called internal reports, must be issued on a monthly basis and a few days before the end of the accounting period (after that, the information becomes outdated and less useful). The lowest frequency for management reports is once every three months.

|

Report |

Monthly |

Quarterly |

Biannual |

Annual |

|

A comparison report between actual and planned performance in the budget for each project |

X |

X |

X |

|

|

A comparison report between the actual and planned performance in the administrative/central budget |

X |

X |

X |

|

|

Cash flow report |

X |

X |

X |

X |

|

Expenditure report |

X |

X |

X |

X |

|

Income report |

X |

X |

X |

X |

|

Financial position |

X |

|||

|

Activity report (result of income and expenditures) |

X |

X |

X |

-

All these reports must be reviewed and approved by the CEO.

-

The organisation must adopt a clear system for its internal distribution process.

A Comparison Report between Actual and Planned Performance in the Budget for Each Project

Actual expenditures are calculated for each budget item and compared with the estimated and planned amounts. The aim of this process is to control the expenditures for each item, while accounting for change, surplus or deficit, if any.

|

Planned performance for the current month D |

Actual performance for the current month E |

Difference between planned and actual performance D-E |

|

|

Telephone |

1000 |

600 |

400 |

|

Travel expenses |

5000 |

5500 |

-500 |

Moreover, this calculation shows decision makers the expenditure areas where the surplus can be used and part of the credit may be transferred to cover the deficit of the remaining sections.

Cash Flow Report

The cash flow report is a cash flow forecast, updated with current monthly receipts and disbursements, as well as any new information about future spending or fundraising plans. It allows managers to anticipate periods in which cash budgets are in a surplus or tend to be insufficient to meet liabilities.

When cash resources are limited, your organisation must take action to mitigate financial difficulties and oversee its ability to pay creditors on time. The options for managing cash flow include:

-

Good credit control: following up with debtors to get them to pay off quickly;

-

Reviewing grant schedules: encouraging pre-payment instead of post-payment;

-

Depositing all funds in the bank on a daily basis;

-

Requesting special payment terms from major suppliers (and insisting on them);

-

Paying some overheads for equipment (e.g. insurance premiums);

-

Prioritising major disbursements;

-

Postponing actions that will lead to additional expenditures, such as employment, vacations and the procurement of equipment;

-

Negotiating an overdraft as a last, yet costly, resort.

Below are the procedures for writing financial reports:

-

The financial department drafts the necessary reports at the end of the financial period.

-

Adherence to all reporting systems and requirements.

-

The director of the financial department conducts a final review of all reports and verifies the differences compared to the estimated budget figures.

-

The financial statements are submitted to the person authorised for approval, and then to the Board of Directors for adoption and validation.

-

The Board of Directors reviews and adopts the financial statements during its session.

-

Reports are submitted for external auditing and kept in a safe place, for a period of 10 years, according to the legal rules in force in Lebanon.

Section 9: Long-term Financial Planning and Sustainability

Civil society organisations need to think strategically and plan on the long term to be able to achieve sustainability.

This requires long-term financial planning, which consists of drafting a plan for primary assets, as well as income and expenditures for a period exceeding one year. The plan shall detail the expected spending for new facilities, utilities, products and other long-term investments by setting a capital budget. It shall also include a cash reserve account for larger future expenditures, such as primary repairs. Likewise, the long-term financial planning shall include an assessment of existing programmes, along with their alternatives, while taking into account new programmes and/or major resource allocations that generally exceed regular allocations.

It is worth noting that CSOs should also explore revenue-generating activities (including investment opportunities), which would allow them to expand their unrestricted resources and ensure better sustainability.

How does the management’s mission and strategy enter into play?

Financial manager are increasingly involved in developing, assessing, and implementing the financial plan. In fact, strategic planning requires effective integration and use of your resources and assets (properties, cash, and even employees) in order to accomplish your mission, noting that this is a one-time action, but rather a continuous practice.

Non-profit CSOs generally do not prioritise profit, but rather serve a cause that transcends financial profit. They adopt a charity cause or seek to improve a situation in society. While a CSO’s programme does not necessarily have to be shut down if it did not generate income, CSOs should ensure the sustainability of their programmes, as this factor can play a decisive role in their autonomy, development, and impact.

What are strategic decisions?

Strategic decisions include developing and rolling out new initiatives or policies. They could be in line with the CSO’s current strategy or with an alternative strategy based on the observed outcomes. While strategic decisions are generally adopted at high level in the CSO’s hierarchy (the Board and organisational team), they could have major consequences on the decision-making process at the lower level. Strategic decisions affect the organisation’s direction as a whole, as well as its objectives and operations. For instance, a strategic decision may entail the provision of services outside the country for the very first time.

Section 10: Auditing

Auditing consists of the independent examination of records, procedures, and activities in a specific organisation, entailing a report on the outcomes. Regular and comprehensive auditing processes generally showcase a CSO’s commitment to transparency, grating it more credibility.

There are two main types of auditing: Internal and External

Internal Audit

Internal audits are carried out within the organisation and include a plethora of inspections, as part of an independent review. This includes:

-

Financial accounting systems and procedures;

-

Administrative accounting systems and procedures;

-

Internal control procedures.

The internal auditor is in charge of reviewing all systems and procedures adopted by the CSO and ensuring they are being implemented correctly, in order to improve operations and bolster internal capacities. The administration receives a report, presents it to the Board, and responds thereto by taking a corrective measure, perhaps by altering a certain procedure or training its cadres.

There are three aspects that affect the internal auditing approach:

-

Economy: not incurring additional costs other than those required for the needed resources.

-

Efficiency: drawing more benefits with less resources.

-

Effectiveness: the CSO’s success depends on meeting its financial objectives and carrying out its mission.

External Auditing

External audits seek to ensure that annual accounts draw a true and honest picture of the organisation’s financial affairs, and that the use of funds is in line with the objectives and goals set forth in the organisation’s mission and vision.

Contrary to internal audits, external audits are often carried out for legal purposes (by virtue of legal requirements) and are often part of the annual review of accounts, or a special review by one of the donors. External audits are carried out by an independent firm employing accountants with recognised professional qualifications, who are not in any way related (personally or professionally) to the organisation nor have a role in its accounting records. Donors can also appoint a special auditor for the project they are funding.

External auditors can also be contracted for other qualitative tasks, such as fraud investigations. While detecting fraud is not the primary objective of auditing, fraudulent actions can actually come to light during the auditing process. Even in this case, auditors must have comprehensive and valid experience, as they will be providing observations on the strengths and weaknesses of operations.

It is worth noting that the time allocated for the auditor to complete their work is limited. As such, the auditor shall focus on validating a random sample of transactions and results, rather than checking the entire accounts. In most cases, the auditor or assessor would want to meet employees, and they may even request to oversee the organisation’s activities as they are being carried out. There is no denying that cooperation during these visits is key and that all necessary efforts shall be exerted in order to ensure that the organisation is honest and transparent about its organisational strengths and weaknesses.

When the auditing date is set, the CSO shall provide the auditor with the following:

-

A calm space where the auditor can work without interruption and/or, ideally, a dedicated room for interviews and other closed discussions.

-

Updated and organised records to facilitate routine audits, minimise work interruptions and reduce on auditing fees.

The following is a template checklist of records and other documents than the auditor may request:

|

Records |

Item Description |

|

A. Basic Accounting Records |

|

|

B. Summaries and Reconciliation Statements |

|

|

C. Sheets |

|

|

D. Other Information |

|

Audit Report

The audit results are set out in a report addressed to the members of the executive time, including and “auditing opinion” regarding the organisation’s current financial and operational position within a specific timeframe. Should the auditors reject the financial results as provided by the organisation, they can draft a report deeming the accounts unsatisfactory. Such a report can be detrimental to an organisation seeking support from donors.

The following table showcases the potential outcomes that an audit report can reach:

|

Auditor’s Opinion |

Comment |

|

No reservations |

Accounts reflect a true and honest vision. Audit report is “clean.” |

|

With Reservations: Subject to |

Accounts are acceptable, with the exception of some issues (such as an incorrect accounting policy, or an undocumented spending item). |

|

With Reservations: Unacceptable |

Several mistakes were committed, the accounts do not reflect a correct and honest vision. |

|

With Reservations: Disclaimer |

Auditors are unable to provide an opinion, as records are extremely faulty or incomplete. |

Should the auditors propose any corrective measures or modifications to the draft financial statements, they must also secure the administration’s approval.

Moreover, auditors oftentimes provide the management with an administration book, which differs from the audit report and highlights the weaknesses found in the internal control systems, along with recommendations for improvement. Directors have the chance to respond to the outcomes listed in the administration book, by explaining the actions they will take to bolster their system and procedures.

Key Terms

|

Term |

Definition |

|

Income |

Total inflows of economic benefits during a specific period. They consist of grants and donations, or any other revenues that the organisation receives as a result of its activities. |

|

Grants |

Local and international assistance provided to the organisation, in cash or in kind. |

|

Running Expenditures |

These consist of salaries, wages, raises and operational expenditures, such as rent, stationery, and electricity, and they cover all of the organisation’s departments. |

|

Capital Expenditures |

These consist of the fixed and capital assets for projects, along the organisation’s other developmental expenses. |

|

Fiscal Period |

A period of 12 months or less, which might or might not correspond to a Gregorian calendar year. The fiscal period starts on the record matching and budgeting date until the next matching and budgeting process. It can also be the period specified in the yearly report. |

|

Budget |

A financial plan organising the organisation’s forecasted economic activities, during the upcoming fiscal period (usually the upcoming year), in quantities and financial values. The plan includes the forecasted income and expenditures during the fiscal period, while ensuring the organisation’s objectives are achieved and detailing the means to do so. |

|

Cash Budget (Cash Flow Plan) |

An estimated budget based, in its drafting, on a cash, rather than an accrual, basis. It showcases the expected income, collected amounts, forecasted cash expenditures, expected external payments, and the cash reserve, on a monthly and yearly basis, at the beginning and end of each month of the fiscal period. |

|

Income and Expenditure Sheet |

One of the key sheets that must be prepared by the end of the accounting period. It aims to showcase the outcome of the organisation/programme/project’s activities, in terms of income and expenditures. Should the income exceed the expenditures, the outcome would be a surplus. However, if the expenditures exceeded the income, the outcome would be a deficit, in which case new sources should be secured to bridge the deficit. The income and expenditure sheet is drafted on an accrual rather than a cash basis. |

|

Funding Surplus/Deficit |

It is the excess of income over expenditures, during the fiscal period. Should the expenditures exceed the income, it would become a funding deficit. |

|

Accounting Entry |

It is the recording and documenting process of an economic event which carries a direct and tangible financial effect on the financial position. The entry is composed of two equal sections: debtor and creditor. |

|

Trial Balance |

A list of all receivables and payables, and their respective balances at a specific point in time. |

|

Cash Inflows |

The total cash flowing into the organisation from any source, including operational, capital or funding-raising activities. |

|

Cash Outflows |

The total cash flowing out of the organisation, irrespective of the spending destination. The latter could include operational, capital or funding activities. |

|

Project |

It is a virtual entity representing an independent and autonomous economic/social activity, with specific independent revenue sources, and specific expenditures aimed at achieving a specific objective which reflects the organisation’s vision. It is dealt with as an independent financial unit. |

|

Funder |

The individual or entity pledging to fund a project or to take part in funding it. |

|

Budget Item |

It is a specific account of a special nature, such as salary expenses for instance, which is included in the organisation’s account structure. |

|

Operational (Current) Expenditures |

These consist of the expenditures serving one fiscal period, such as the organisation’s regular expenses (salaries, stationery, phones, etc.). Capital expenditures, on the other hand, represent expenses that serve the organisation for more than one fiscal period, such as: purchasing fixed assets. |

|

Assets |

In general, these are the organisations properties, which help it generate income. They include current and fixed assets, among others. |

|

Payment Receipt |

A template clarifying the payment data: Name of the beneficiary, date, amount, beneficiary’s signature, treasurer’s signature, and type of payment. The document should be systematic, numbered in advance, and issued in several copies. |